Multifamily - What’s Ahead for 2026?

Hey Team,

It’s 17 degrees outside as I write this, and I think I can speak for most of us when I say we’re grateful the weekend storm didn’t end up being as severe as originally forecasted. Hopefully everyone stayed safe, warm, and has all their water pipes still intact.

Let’s jump in!

Capital Markets Update:

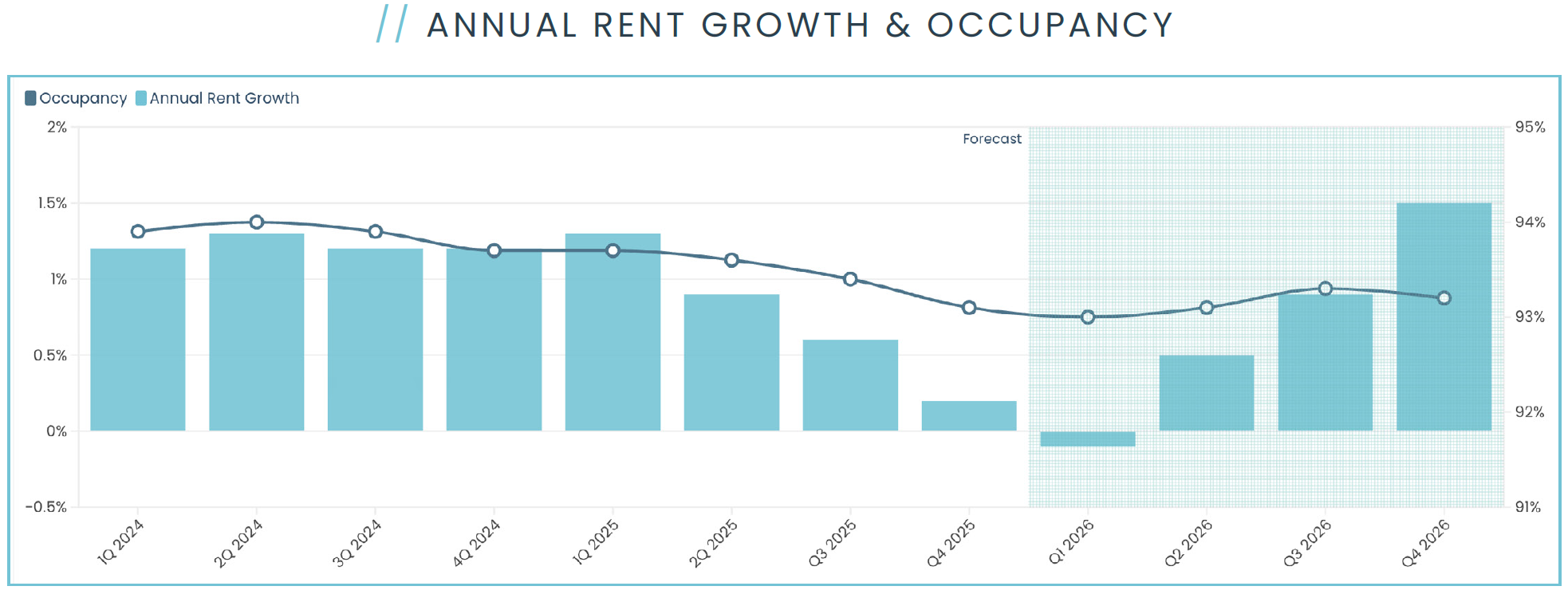

Last year (2025) was initially perceived as a year of stabilization for the US multifamily market because of strong absorption, early rent growth, and steady occupancy. Unfortunately, those early indicators were short lived. Starting in Q2, occupancy started to slip, rent growth compressed, and owners began offering concessions largely due to the softening labor market. Just last week we noticed the following concession packages in our local market:

2 Months Free AND a Nespresso, Robo Vac, or TV

6 weeks free rent

2 months free

$125 off rent & free application

I could use a new coffee maker, do you think I could talk my wife into moving to an apartment!?

Looking ahead at rent growth and occupancy trends, the national outlook is best characterized as a gradual, uneven recovery rather than a clean reacceleration. The supply pipeline is thinning materially, which should reduce competitive pressure as 2026 progresses, but the market continues to contend with elevated vacancy across many metros and ongoing sensitivity to labor-market momentum.

*MMG 2026 Forecast Report

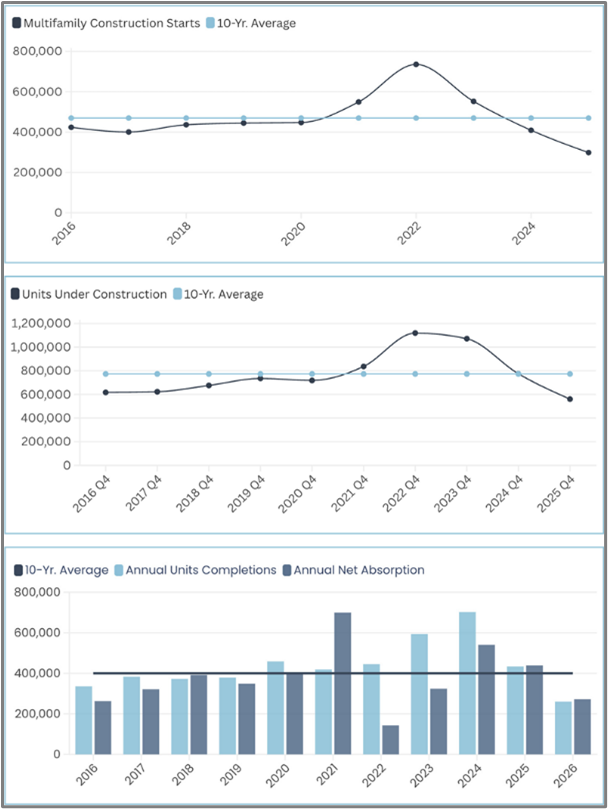

Speaking of thinning supply, the U.S. apartment market is moving into 2026 with the development cycle firmly past its peak.

After a heavy wave of deliveries in 2024 and 2025, new construction is now slowing, and we’re beginning to see a sustained pullback in unit completions.

Nationally, multifamily deliveries are expected to fall to roughly 260,000 units in 2026, a meaningful step down from recent highs.

*MMG 2026 Forecast Report

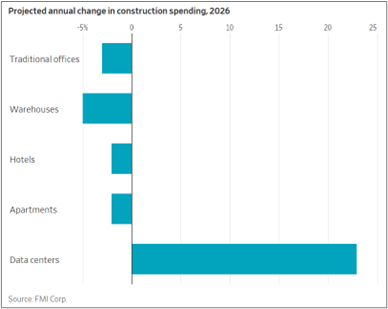

With apartment development cooling, where has the construction market shifted?

Spending on data centers is set to jump 23% in 2026, rising from 2% to over 6% of the nonresidential construction market. Tech giants like Amazon, Google, and Oracle are investing billions in AI-ready facilities—undeterred by rising costs.

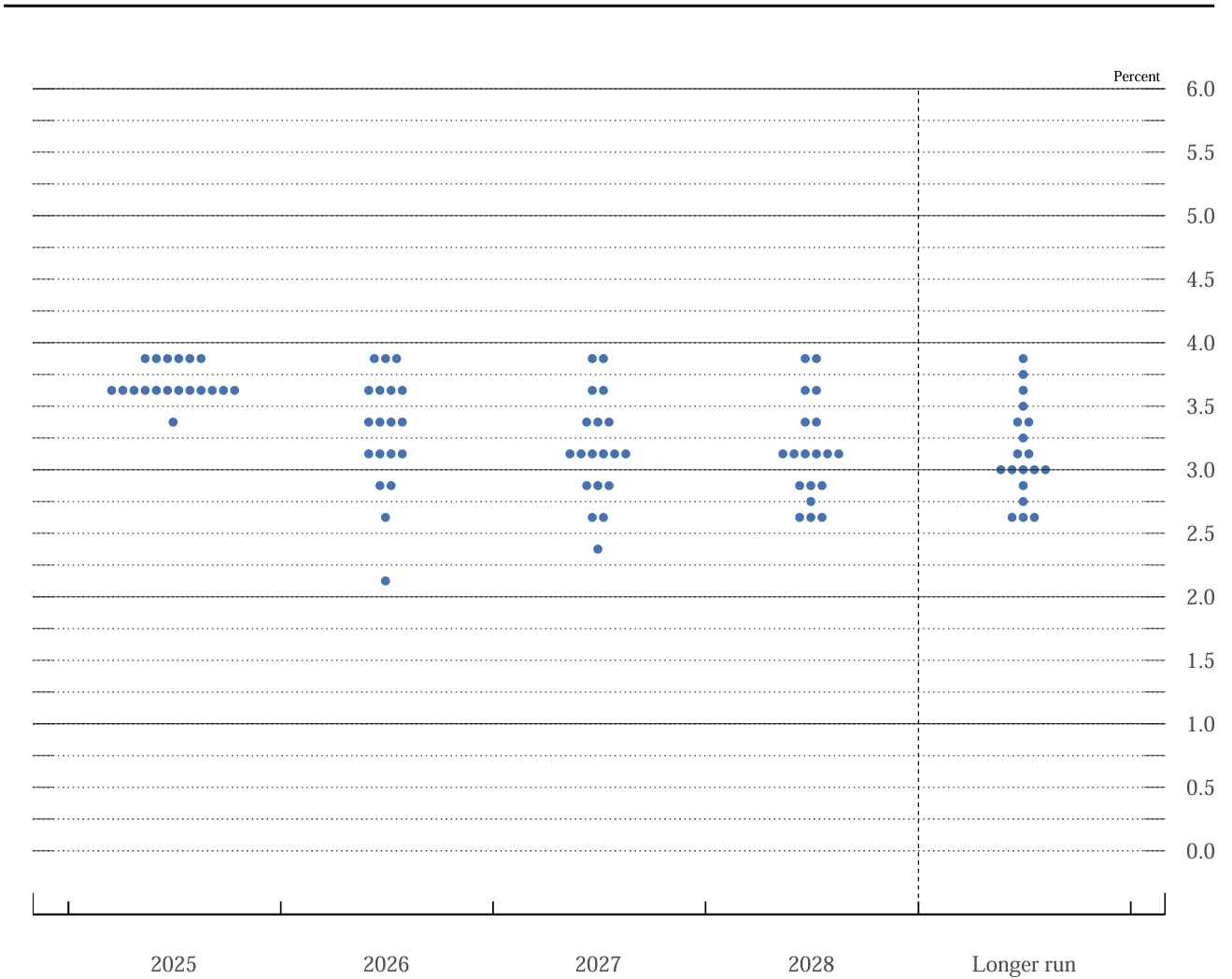

The Federal Reserve’s current target range for federal funds rate is 3.5%-3.75%. This range was set at the December 10, 2025, meeting which reduced the target rate 25 bps. According to the latest dot plot, the target fed funds rate will likely settle between 3.0%-3.75% with a stable outlook for the next several years.

December 10, 2025

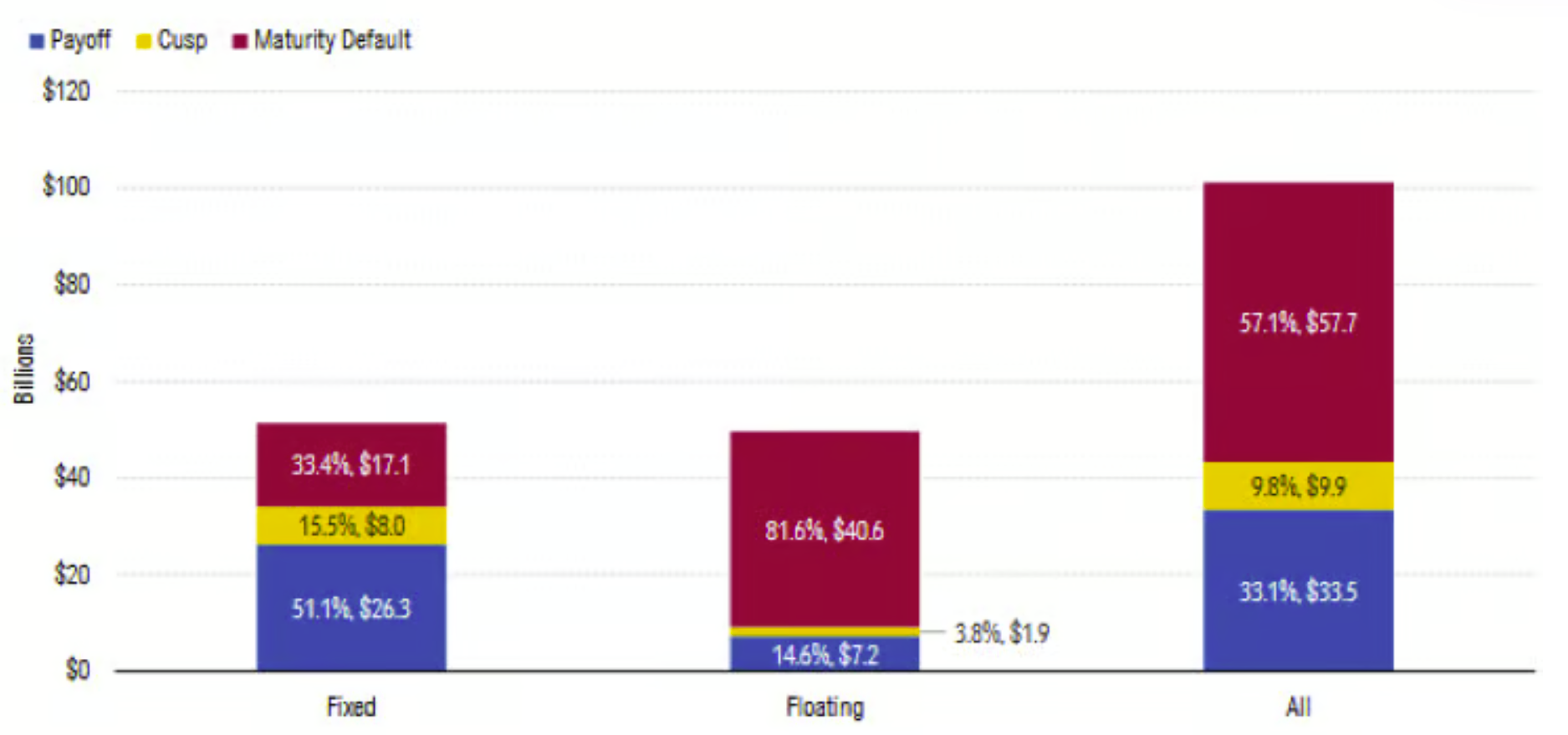

According to Intex and Morningstar, over $100B in CMBS loans mature in 2026, with over half likely to miss repayment. Instead of widespread defaults, many will be modified—historically a lower-loss path that gives borrowers time to recover.

510 Capital Update:

We closed on an extremely attractive cash-out-refinance at one of our properties in Hendersonville, NC. In total, we have returned over 170% of our investor’s initial capital for this project. We’re eager to put this capital straight to work, if you have an investment opportunity available, please let us know.

Our take on the market is that 2026 could provide solid multifamily investment opportunities for both developers and value-add investors. Short term market turbulence creates weakness in the market.

Our philosophy is to buy into weakness when liquidity is tight and sell into strength when liquidity is flowing. A shrinking supply pipeline and a more stable rate outlook strengthen the case for well-capitalized, disciplined development, assuming cost-to-build can be controlled. Additionally, if 2026 can provide modest rent growth and increased occupancy, the feasibility of value-add acquisitions increases.

In Western North Carolina, the market is still digesting new supply. About a year ago, I made the “Field of Dreams” comment— “If you build it, they will come”—when talking about housing demand in WNC. That long-term demand story is still intact, but in the short term it’s played out as we predicted in one of our earlier newsletters: rents have stayed relatively flat, and leasing has been more challenging as operators work through the recent wave of new units.

The Upstate of South Carolina experienced a similar supply-driven dynamic but appears to be further along in the absorption cycle. We’re now seeing early signs of stabilization, with modest rent growth and improving occupancy as the market works through recent deliveries. Again, it’s played out as we predicted in one of our earlier newsletters.

Notable Reads:

Ryan’s Pick

Extreme Ownership by Jocko Willink. This book reads like an action movie as Jocko goes through leadership examples he dealt with in Iraq. The big lesson I learned is to take ownership no matter what. Even when it seems justified to blame someone else or when circumstances were seemingly outside of my control, by choosing to take ownership, it rewires my brain to solve problems and improve as a leader and business owner.

Luke’s Pick

Fundamentals by Michael Huseby is a clear, methodical walkthrough of how investment funds and real estate syndications are structured.

It’s dense, technical, and extremely thorough… so fair warning: if you’re having trouble sleeping, a few pages might do the trick. Jokes aside, it’s an excellent resource if you’re serious about forming a fund or running syndications the right way.