Everything’s Changed - Pros vs Joes

In the most recent real estate investment bull run from 2010 to 2022 there were a few unique factors that contributed to that investment environment.

1. Historically low interest rates and compressed cap rates – IE cheap money and inflated values

2. Retail capital was loose and readily available – IE massive amounts of liquidity

3. Anybody that could sign a closing statement could make money and look like a savant

4. Real estate investors rallied around “hype” instead of expertise and strong market fundamentals

“Luck” (unfortunately mistaken for macroeconomic tailwinds) favored the bold – until it didn’t. Everything’s changed. Retail liquidity has tightened up, lines are being drawn between real estate professionals and amateurs, and – in the long run - industry expertise and institutional experience will beat luck. If real estate were easy, everyone would do it. We have a lot to catch up on, let’s jump in!

Capital Markets Update:

A lot has been said about the One Big Beautiful Bill, but in case you missed it, here are the highlights for real estate investors!

100% Bonus Depreciation Restored & Permanently in Place - You can now fully expense qualifying short-lived assets (e.g. HVAC, lighting, site improvements) in the first year for property placed in service from Jan 20, 2025, through at least 2029. This accelerates tax deductions and improves early cash flow through cost segregation strategies. Our team always completes a cost segregation study upon acquisition to ensure our investors take full advantage of bonus depreciation.

Expanded Section 179 Expensing Limits - Increases the expensing cap to $2.5M with phase‑out kicking in at $4M—this amplifies write‑off potential for qualifying assets.

Permanent Qualified Business Income Deduction - Up to 20% deduction on income from pass‑through entities and REIT dividends. Previously set to expire after 2025, it’s now permanent.

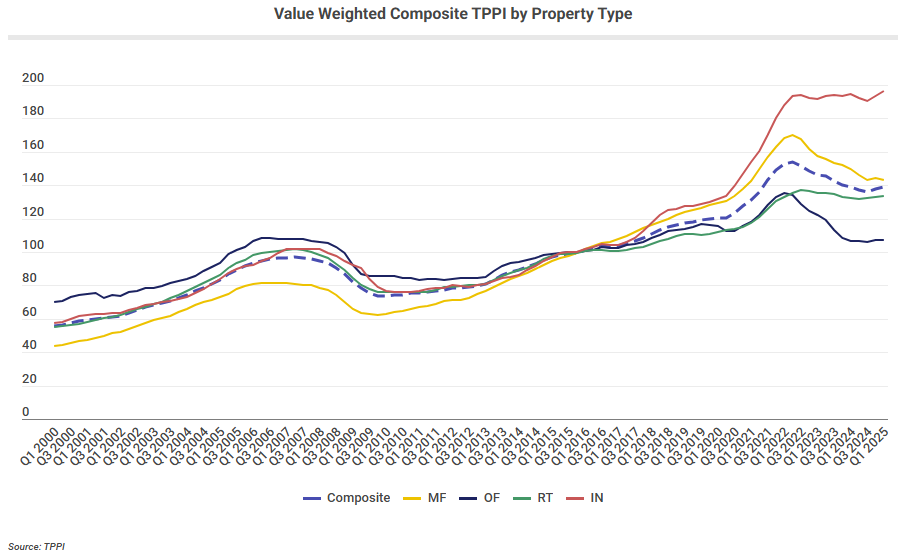

The Trepp Property Price Index (TPPI) highlights significant shifts in asset performance across sectors (multifamily, office, retail, industrial). Since peak pricing in 2022, industrial has maintained strong values, reflecting continued demand for logistics and warehouse space.

All other asset types have seen a 15–35% correction but seem to be leveling out as the market adjusts to higher interest rates and tighter capital conditions. For investors, this signals potential buying opportunities in sectors that have corrected but retain strong fundamentals.

The multifamily market is in the midst of a significant reset. National rent growth remains muted at just 1.3% year-to-date, far below historical norms, as excess supply—particularly in Sunbelt metros like Austin, Denver, and Phoenix—continues to pressure rents. Despite this short-term softness, the fundamentals for a recovery are forming. New apartment completions are dropping sharply while demand for rentals remains strong, driven in part by persistently high mortgage rates that keep more households renting. This supply-demand imbalance is expected to ease by late 2025 or early 2026, setting the stage for stronger rent growth in the following years.

RentCafe’s Best Places for Renters to Live in 2025

Rankings reflect a clear shift in renter preferences. Southern cities now dominate the national landscape. Out of 150 cities analyzed, 41 Southern metros ranked for affordability and livability. Why It Matters - Renters are increasingly prioritizing a balance between affordability, opportunity, and quality of life.

Remote work continues to reshape housing. Cities in Texas, Florida, and the Carolinas are boosting infrastructure and housing to meet growing demand from renters nationwide. Highlighting our markets below…

#19 Greenville, SC

#43 Asheville, NC

#49 Spartanburg, SC

Rent Payments Hit New Low for Independent Landlords

On-time rent payments slipped to 83.6% in July, continuing a two-year decline and marking the lowest trend since the pandemic. Even with only a slight dip from June, the overall forecast for full payments dropped to 93.4%, its weakest since 2020. Small multifamily units performed best at 84%, while larger buildings lagged at 82.4%—the widest gap in over a year.

Rising consumer debt and delinquencies are adding pressure, making timely rent payments harder for many tenants. Currently at 510 Capital, we focus on the basics - making sure our buildings stay full, tenants are well screened, and rent comes in on time. As long as we continue to do our job well, we will weather whatever the market throws at us.

Reshoring Impact

I ran across this chart a couple weeks ago and thought it was fascinating. While some data seems particularly difficult to quantify, the thesis tells a compelling story for capital investment in the Carolinas.

The impact of 'reshoring', where companies bringing jobs back to the U.S., bodes well for our region. South Carolina stands to gain an estimated 25,000 jobs, with North Carolina also adding over 5,000.

It simply highlights the growing economic activity and the strong workforce we have right here in our backyard. We continue to feel good about what this trend means for our portfolio and the ongoing growth we're seeing in the area.

Multifamily Occupancy

Multifamily occupancy across the board continues to stabilize. Class A apartments reached 95.7% in May 2025, the highest since June 2022 and a 1.7% jump year-over-year, the largest gain among apartment classes. Though Class A slightly trails Class B (95.8%) and Class C (95.6%), it has now surpassed its pre-pandemic average of 94.7%. Historically, Class C led occupancy, but that shifted in late 2023 with Class B taking the lead. Class A has faced challenges from new supply and resident turnover, but improving demand means all classes are now above pre-pandemic norms.

I’m excited to share my favorite graph plotting CRE transaction volume and cap rates. While we’ve seen a slight increase in transaction volume, the stability suggests CRE may finally be adjusting to higher interest rates and moving past pandemic-driven disruptions. Additionally, deals are still getting done!

Let this sink in: According to Trepp, over the next 18 months, $115B in commercial real estate loans with sub-1.20x debt service coverage ratios are set to mature, with multifamily loans standing out as the largest slice of upcoming maturity volume (30.9%, or $35.45 billion). There is more pain to come, but also opportunity.

510 Capital Update:

Recently, we had the opportunity to share some “before” and “after” photos from one of our projects with our investors. In fact, Ryan and I had a conversation with one of our tenants at this property a couple months ago. Ryan simply asked, “Is everything ok with your apartment?” The tenant responded, “Yes! I love it here!” I find personal satisfaction knowing that we can transform distressed units into clean, safe, affordable housing for our tenants.

Notable Reads

Ryan’s Pick:

The Obstacle is the Way by Ryan Holiday. This is a great reminder that so often we chase comfort and try to avoid difficulty, but a lot of the time, success, growth, and fulfillment come from going through hard things rather than trying to avoid them.

Luke’s Pick:

The Anxious Generation by Jonathan Haidt, PhD. This book hit home for me as a parent of two young boys. Haidt unpacks the dramatic shift from a play-based childhood to today’s screen-based childhood and how that transition has fueled the rising tide of anxiety among younger generations. It’s an eye-opening look at the sources of this problem and the long-term impact on kids’ mental health and development. If you’re a parent, grandparent, or simply invested in the next generation, these ideas are need-to-know.

If you’d prefer a high-level summary, I found a great interview with the author that touches on the main ideas. Link below: