Multifamily - Renewed Momentum ? 👀

Hey Team,

After navigating a sharp reset from the 2022 valuation peaks, the US multifamily real estate sector is entering the final stretch of 2025 with indications of renewed momentum despite macroeconomic headwinds.

The Federal Reserve cut rates 25 bps in September and October marking the central bank’s range at the lowest level since December 2022.

Multifamily valuations have finally returned to positive territory (more commentary on this below).

The recently passed One Big Beautiful Bill Act restored 100% bonus depreciation making real estate investment more appealing for savvy investors.

Let’s jump in!

Capital Markets Update:

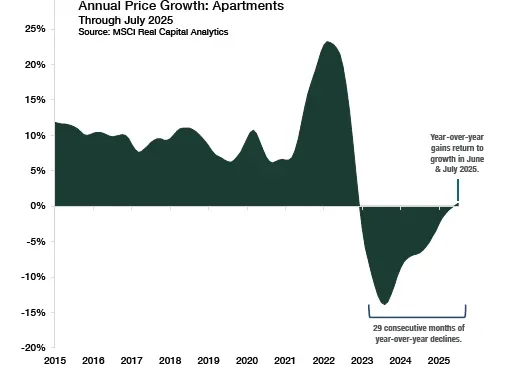

Multifamily valuations had declined roughly 19% since 2022, or over 26% when adjusted for inflation. By mid-2025, according to Real Capital Analytics those values have finally returned to positive territory. This marked the end of 29 consecutive months of year-over-year losses.

The Southeast U.S. is experiencing an unprecedented wave of capital investment, with companies building new factories, data center campuses, and logistics hubs across the Sun Belt. The region expects $264.7 billion in total investment, which will generate about 150,349 jobs. This pipeline is concentrated in EV battery manufacturing, clean energy infrastructure, data centers, aerospace and defense, and transportation logistics.

Apartment demand pressure is expected to ramp up 12–24 months after major project announcements, providing a window to acquire or develop assets ahead of the leasing wave. Watch secondary markets like Bowling Green, KY, Clarksville, TN, Spartanburg, SC, Athens, GA, and suburban Richmond, VA.

More than $264.7 billion is earmarked for projects through the late 2020s, with the largest commitments in Louisiana, Virginia, Tennessee and North Carolina. In summary, one new job typically supports about 1.5 additional people in the local population. This “people-per-job” multiplier, confirmed by decades of studies, means job growth drives population growth as workers—and often their families—move in. Many newcomers are renters, especially at first, so each job created boosts demand for rental housing. Housing economists and HUD studies stress the need to build housing in step with job gains. Planning for about 1.5 people per job helps keep employment growth and housing supply in balance.

The CMBS Special Servicing Rate, a key indicator of loan distress, rose to 10.65%, the highest level since 2013. While this reflects growing stress in parts of the commercial real estate market, particularly office and retail, the multifamily sector remains relatively stable compared to other property types. As of the end of September, multifamily maintains the lowest special servicing rate of all asset types.

Single-family permitting has fallen to its lowest level since 2023, when 30-year mortgage rates last peaked above 7.6%. This decline indicates that home builders are scaling back new projects in response to elevated borrowing costs and ongoing affordability challenges. At this stage in the economic cycle, the housing market appears to be in a cooling phase following several years of rapid growth and cost inflation. For builders and developers, the focus has shifted from expansion to operational efficiency—completing existing projects, managing cash flow, and preserving liquidity. While near-term activity may remain muted, this environment can create opportunities for well-capitalized developers to acquire land or projects at a discount, setting the stage for future growth once interest rates moderate and demand stabilizes.

Lending momentum has rebounded meaningfully in 2025 after a sharp pullback over the past two years. While activity remains below the 2021–2022 peak, the index shows clear signs of stabilization and renewed appetite from lenders. This reflects improving capital market conditions, with borrowers and lenders re-engaging as interest rate expectations become more predictable. Overall, momentum is normalizing, suggesting healthier liquidity compared to the trough of late 2023.

After several quarters of steady occupancy near 93.7%, softening renter demand modestly reduced occupancy in Q3 2025 to 93.5%. While the peak of new apartment supply is now in the rearview mirror, the ongoing lease-up of recently completed projects continues to exert pressure on occupancy. However, as these properties stabilize and the market moves further from the delivery peak, occupancy and rent growth is expected to gradually improve through 2026.

For my friends in office, industrial, and retail space. The Boulder Group highlights expanding cap rates for office investors but steadying/compressing cap rates for industrial and retail sectors – emphasizing investor confidence and perhaps settling into a new normal.

In Summary: Ryan and I believe we’re in a unique window of opportunity for multifamily investment. Occupancy levels have stabilized, and new supply is being absorbed. We expect both occupancy and rent growth to improve through 2026.

Additionally, the recent shift in interest rate policy is creating a more favorable lending environment, which we anticipate will drive renewed investor activity and gradual cap rate compression. Together, these dynamics point toward a period where well-timed, strategic acquisitions can benefit from both improving fundamentals and rising asset values.

510 Capital Update:

We’re under contract! This month we contracted on a small, off-market, 12-unit property in Greenville, SC. We’re really excited about this property – the location is great, the product is well constructed, and the basis is very attractive. Since this deal is “bite-sized”, we offered it to our current list of active investors first and we were fully committed within the week. What’s the adage – “good deals find capital.” That said, we’re thankful for your partnership and we’re excited to provide more details once we close.

Our team is continually sourcing new investment opportunities. As part of our network, you’ll have direct access to those offerings as they become available. We value the relationships we’ve built with our investors. If you know someone in your network who shares a similar interest in real estate investments, we’d welcome the opportunity to connect and explore whether our upcoming projects might be a good fit for them as well.

PS, if the charts or data presented above is helpful for you or your network and you’d like more info, I’m happy to share the source data/reports and we can nerd-out together!

Notable Reads:

Ryan’s Pick:

Thinking in Bets by Annie Duke - This is a great book that compares life to poker, where there is an element of chance and things outside our control, but an ideal way to play each hand. We can play our "hand" right and lose and we can play our "hand" wrong and still win. Great poker players have the ability to see past the outcome itself. This book really shaped how I look back at past decisions and try to learn from them and improve.

Luke’s Pick:

“Wall Street is a street with a river at one end and a graveyard at the other.”

Liar’s Poker by Michael Lewis is a semi-autobiographical account of his experience as a bond salesman at Salomon Brothers during the 1980s Wall Street boom. The stories he tells are thrilling, absurd, and generally capture the greed, hubris, and borderline (or not) illegal culture of high-stakes traders. This one is just fun!