Is Multifamily at a Turning Point?

Hey Team,

The 2026 apartment market looks better on paper, but on the ground, it’s still sluggish. Oversupply and concessions are muting rent growth, but there are early signs the market may be approaching a turning point. Rent growth is the engine that drives multifamily, so let’s start there.

Capital Markets Update:

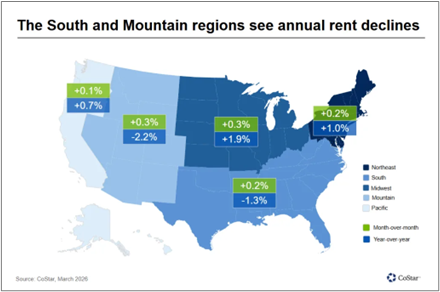

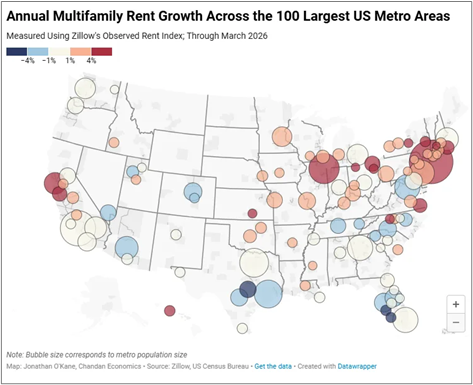

CoStar data shows a clear picture of multifamily rent growth by region. The Southeast is seeing modest month-over-month rent growth, but remains negative year-over-year, reflecting the impact of recent supply and broader economic pressure, which we’ve covered at length in previous newsletters.

This aligns with what we see across our portfolio, where rent levels have softened compared to last year despite some stabilization. Encouragingly, leasing activity is picking up as we move into the stronger spring and summer leasing season.

So, what’s driving that rent growth outlook?

It comes down to supply.

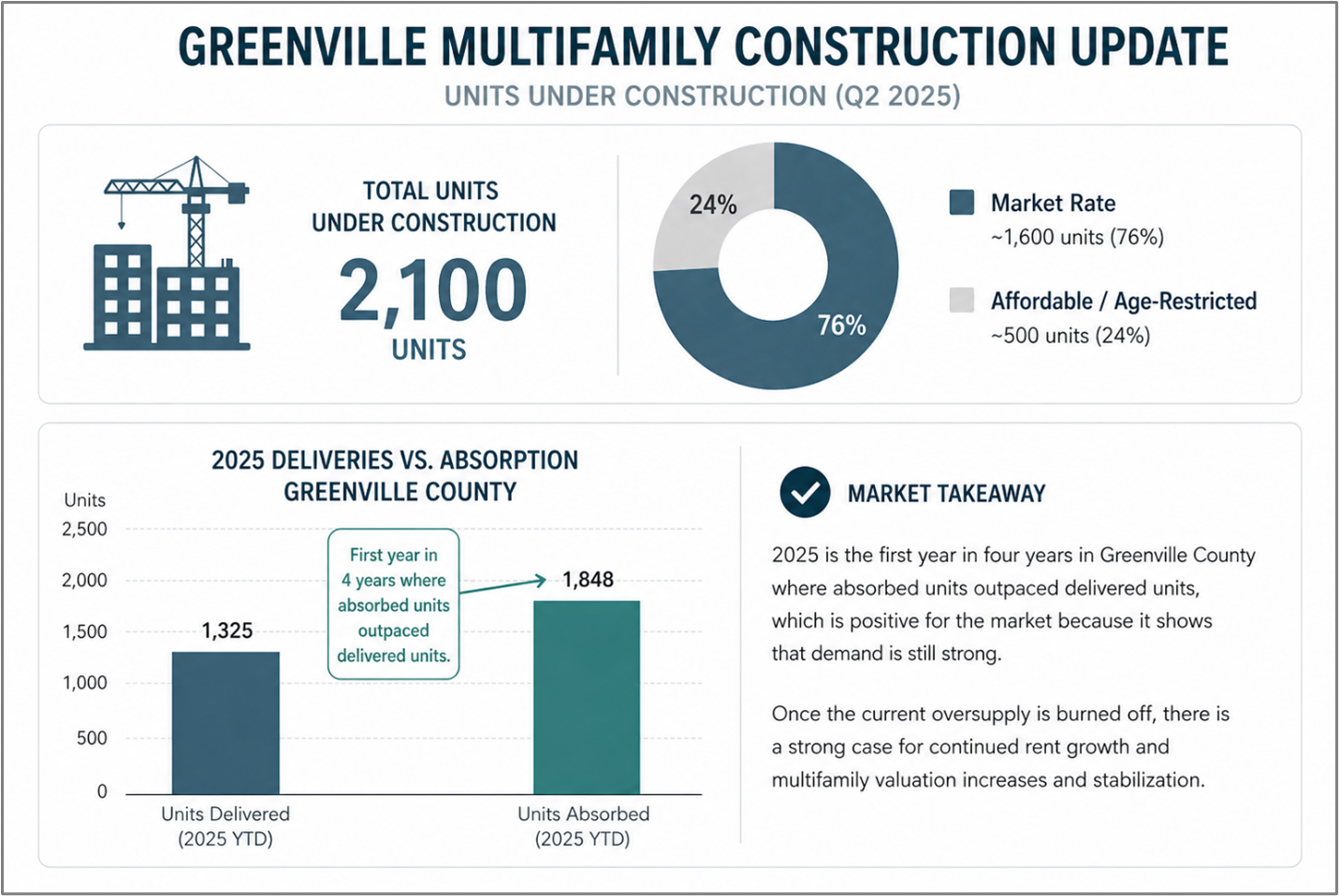

In Greenville, we’re finally starting to see demand catch up.

This is not an issue specific to Greenville (or western North Carolina), we are seeing supply trends normalize across the Country.

This is a classic case of basic economics. Once demand outpaces supply, we will begin to see rent growth again.

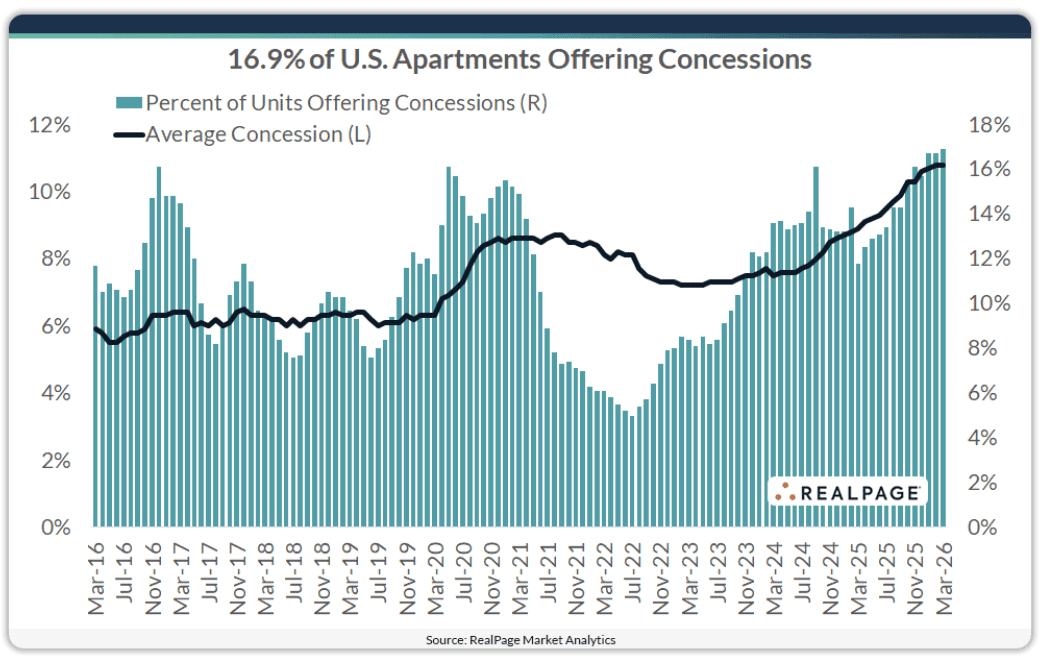

Another result from the over supply mentioned above is elevated concession activity. Concessions have climbed to a 10-year high, with nearly 17% of units nationally offering discounts and average concessions equating to roughly six weeks of free rent. The pressure is most pronounced in workforce housing, where over 21% of Class C units are offering concessions, and in the South, which leads the country at just over 21%. This reinforces what we’re seeing across the Southeast—supply-driven pressure is forcing landlords to prioritize occupancy over rent growth.

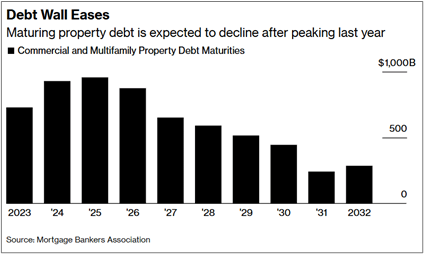

Commercial and multifamily mortgage maturities (AKA The Debt Wall) are projected to drop 9% in 2026 to $875B, down from $957B last year, according to the MBA, with annual totals expected to keep declining through 2031. The debt wall isn’t gone, but it is shrinking. As maturities ease and originations rise, 2026 looks more like a transition year than a cliff.

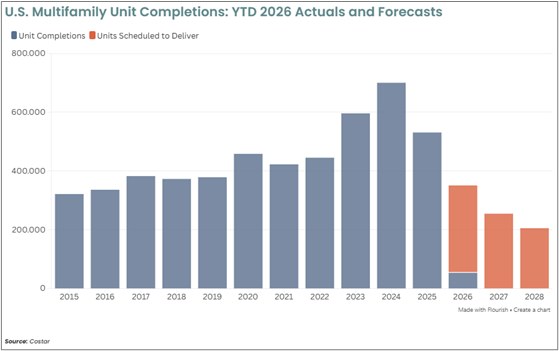

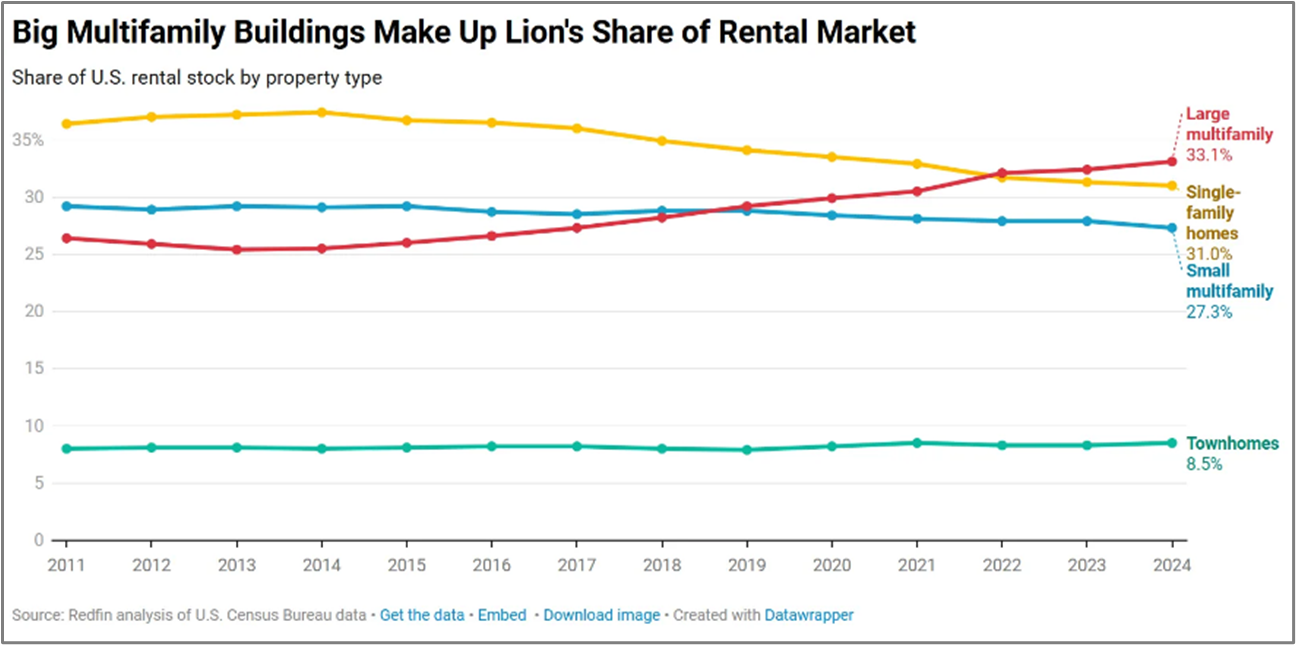

The rental market has changed drastically in the last 15 years in terms of “type” of rentals available. Multifamily construction surged in recent years, pushing total units to record levels and giving renters more options—ultimately putting pressure on rent growth. Meanwhile, single-family construction hasn’t kept pace and much of it goes to owner-occupants, keeping the rental supply tight. As a result, multifamily offers scale and stability, while single-family rentals continue to command a premium.

A record 25.2 million young adults (ages 18–34) are living at home, which is now above peak Covid levels. The narrative is that job availability is the issue and that this will be a real headwind for multifamily demand in the near term. I don’t fully buy that. From my perspective, there are plenty of opportunities for people willing to show up, be flexible, and work (I’m excluding those who are unable to work because of various uncontrollable challenges).

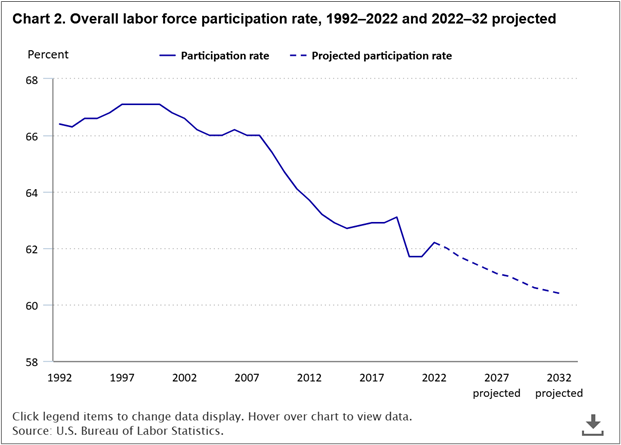

At the same time, labor force participation has slipped to 61.9% (down 60 bps), well below the 67.3% peak in 2000. The biggest participation rate drops were seen among those ages 55 and older and those between the ages of 20 and 24 (see graph below).

The takeaway: this isn’t just an economic issue—it’s behavioral. Over the long term, household formation won’t disappear, but it will likely get delayed.

Personally, I think about this in terms of my kids and how I’m trying to raise them. If I can teach discipline, responsibility, a willingness to show up and work hard and treat other with respect, they’re already ahead of a large portion of the population. With labor force participation near multi-decade lows, the bar isn’t that high. There’s real opportunity for the next generation who are willing to take some initiative and live a purpose driven life.

Alright, I’ll step off the soapbox 😏… back to the newsletter.

510 Capital Update:

Potential Acquisitions: Q1 2026 has been the slowest stretch for acquisitions Ryan and I have seen since we started in 2017. Deal flow has been limited, and what’s out there largely hasn’t penciled. But we’ve stayed disciplined, even as many of the same deals from prior years resurface with no improved outlook. That said, we’ve started underwriting a few new opportunities we’re excited about, and we believe 2026 could shape up to be a more attractive buying environment - more on that in Luke’s Picks at the end.

Capital Projects: We recently completed a few capital projects across the portfolio. Why? Because we invest with a long-term lens. These improvements support property longevity, tenant safety, and curb appeal, all of which drive retention over time. Below is a recent parking lot seal and stripe, we think it turned out great! What do you think?

Market Blurbs:

In Western North Carolina, the story is similar to last quarter. We are still working through new supply and market headwinds, but our long-term perspective is bullish for the area.

The Upstate of South Carolina seems to be at the tail end of the cycle. We’re seeing strong absorption and supply is beginning to normalize. We expect to see modest rent growth within the next 12 months.

Notable Reads:

Ryan’s Pick:

Crushing it in Apartments and Commercial Real Estate by Brian Murray: One of the books I read early on, as we started scaling into apartment buildings. It's easy to read with real case studies on how to be successful and avoid pitfalls in this business. As we navigate these market cycles, these core fundamentals are critical to ensure long-term success in this business.

Luke’s Pick:

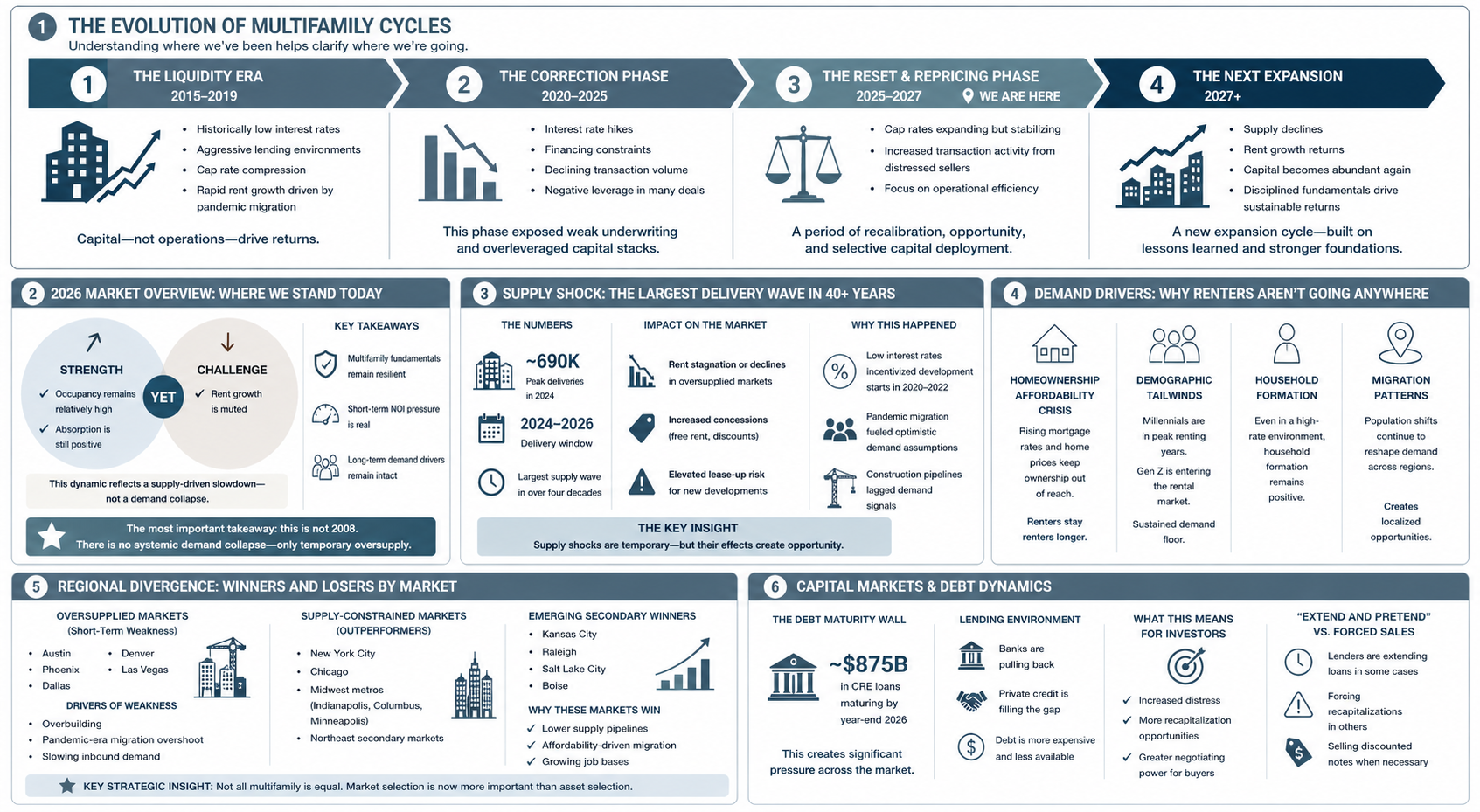

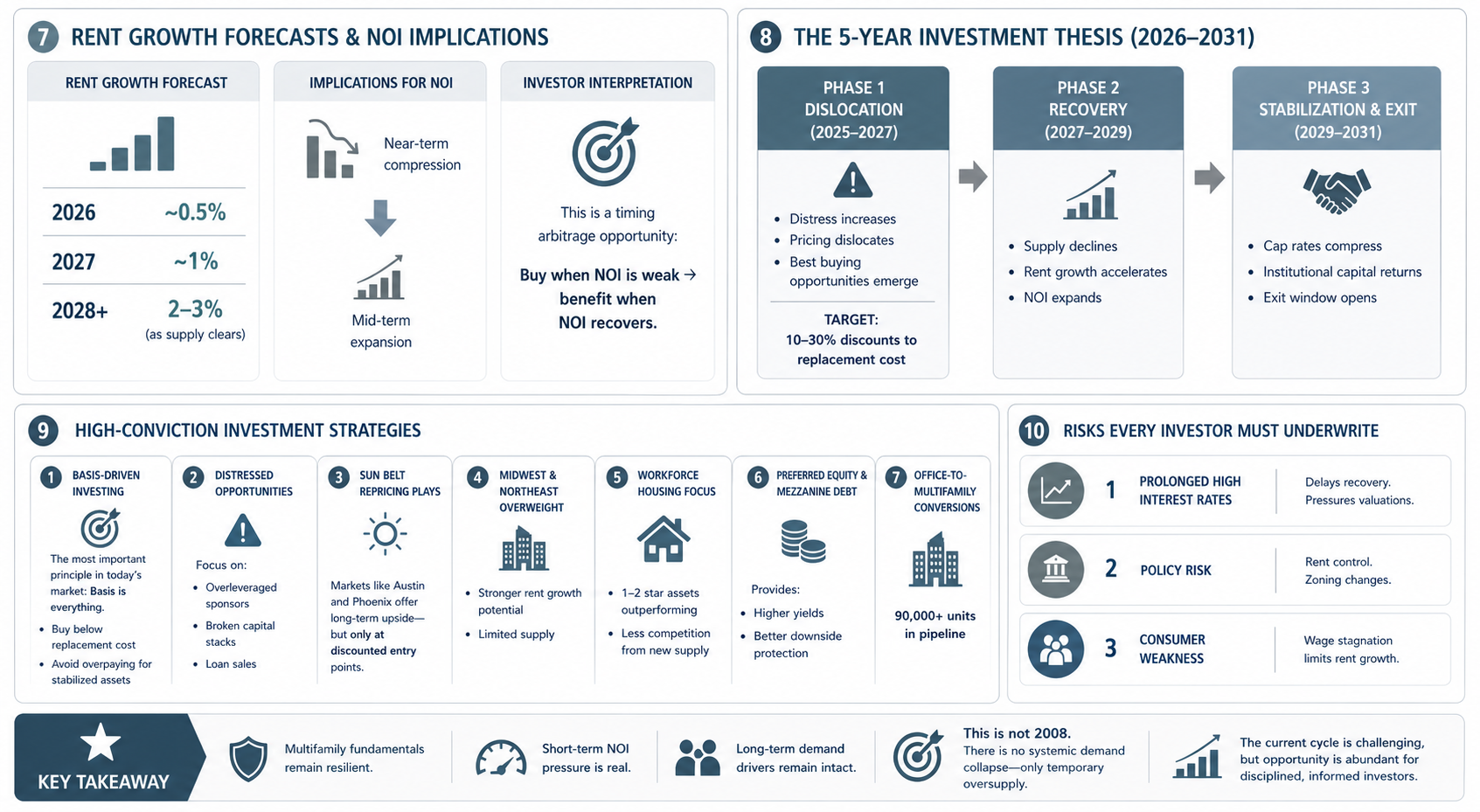

Switching it up this quarter…no book recommendation. I put together a simple, visual breakdown of the multifamily cycle to answer these questions:

Where have we been?

Where are we now?

Where are we going?

What do we think about the multifamily cycle?

It’s quick, practical, and I think it’ll help you connect the dots on what’s actually happening in the market. I think this is something my dad would put together - shout out dad for simplified handouts!

As always, we appreciate your partnership.

Till next time,

Luke